Economic Policy Papers are based on policy-oriented research produced by Minneapolis Fed staff and consultants. The papers are an occasional series for a general audience. The views expressed here are those of the authors, not necessarily those of others in the Federal Reserve System.

In its “Statement on Longer-Run Goals and Monetary Policy Strategy,” the Federal Open Market Committee (Federal Reserve Board of Governors, 2014) summarizes its two main objectives: to mitigate (i) deviations of inflation from its longer-run goal and (ii) deviations of employment from the Federal Open Market Committee’s assessment of its maximum level. In the case of employment, the statement acknowledges that “the maximum level . is largely determined by nonmonetary factors,” which is why the FOMC sets no fixed goal for the employment level. It instead depends on the Committee’s “assessment.”

In this paper, I investigate the link between monetary policy and employment using predictions of current monetary theory. The results show that even with the extraordinary monetary accommodation provided by the Fed since 2008, theory predicts only a small impact of monetary policy on employment. Other research suggests that to understand what does impact employment levels and hours worked, economic theory should be modified to account for factors that impact labor-leisure decisions.

Prior to the financial crisis of 2008, the conventional tool of the Federal Reserve was adjustment of the federal funds rate, the interest rate charged on overnight loans between banks holding funds at the Federal Reserve. During the financial crisis, the Fed lowered this rate to nearly zero. It then used tools it considered “unconventional”—specifically, a wide range of credit market interventions—with the goal of adding further liquidity to the economy.

This change in policy—from the Fed’s conventional use of fed funds rate adjustments to its unconventional interventions in credit markets—is reflected in the theoretical models now used by monetary economists to analyze the effects of such policies. Models of “conventional monetary policy” assume the Fed controls interest rates; models of “unconventional monetary policy” assume the Fed intervenes in credit markets. In this section, I briefly review the main predictions of conventional models and then discuss the predictions of unconventional models for employment during and after the financial crisis.

Models of conventional monetary policy

According to models of conventional monetary policy, policy has an impact on real (adjusted for inflation) activity such as employment because it is assumed that prices of goods don’t adjust instantly in response to Fed policy changes. If prices are already printed on a menu or store catalog, for example, prices can be slow to adjust (or “sticky”) following a change in Fed policy because it takes time to reprint menus with updated prices that reflect the policy change. And when firms do physically update their prices, they may act strategically—choosing to change prices only a small amount—for fear of losing business to other firms if those firms haven’t yet adjusted their prices. The smaller the firm’s price change response—due either to strategic decisions or to the realities of adjusting physical price lists—the larger the impact of monetary policy.

In Chari, Kehoe and McGrattan (2000) and McGrattan (1999), we computed outcomes of a sticky prices model to determine the impact of Fed policy on real activity. We found that the impact is short-lived; once firms have the opportunity to update prices, they do so and there is little or no strategic delay. 1 In other words, soon after the policy change, the time series from our model economy look as they did before the change. Furthermore, if we feed in actual changes to the Fed funds rate, the model and actual time series are not closely aligned. As a result, we concluded that Fed conventional monetary policy is not the main driver of U.S. business cycles.

Regardless of these results, analyzing Fed policy after 2008 presented new challenges to monetary theorists because their existing models did not reflect the unconventional tools—credit market interventions—used by the Fed beginning in the fall of 2007. New theory and new models were needed to understand these new monetary policy tools.

Models of unconventional monetary policy

There has been a surge in theory development and model building since the 2008 downturn. Macroeconomic models, in particular, have been modified to include the financial market disruptions that prompted Fed action. 2 Here I consider Gertler and Karadi’s (2011) model which incorporates the Fed’s direct involvement in credit markets.

The Gertler-Karadi model assumes that all household investment is “intermediated” by financial institutions such as commercial banks. This means households deposit funds at these banks, which then lend the funds to firms. The model also assumes that bankers are no longer bankers after a specified number of years and can divert some of the household deposits into large bonuses for employees and dividends for shareholders. 3

To mimic financial market disruptions that lead to large declines in the net worth of financial intermediaries, Gertler and Karadi model a financial crisis as a large, negative shock to the quality of the capital (or assets) held by intermediaries. When a crisis occurs, the spread rises between returns on business capital and household deposits. To reduce this spread, the Fed injects additional credit into the economy—that is, it intervenes in credit markets. Negative shocks continue in the model for two to three years after the initial shock, but with diminishing severity.

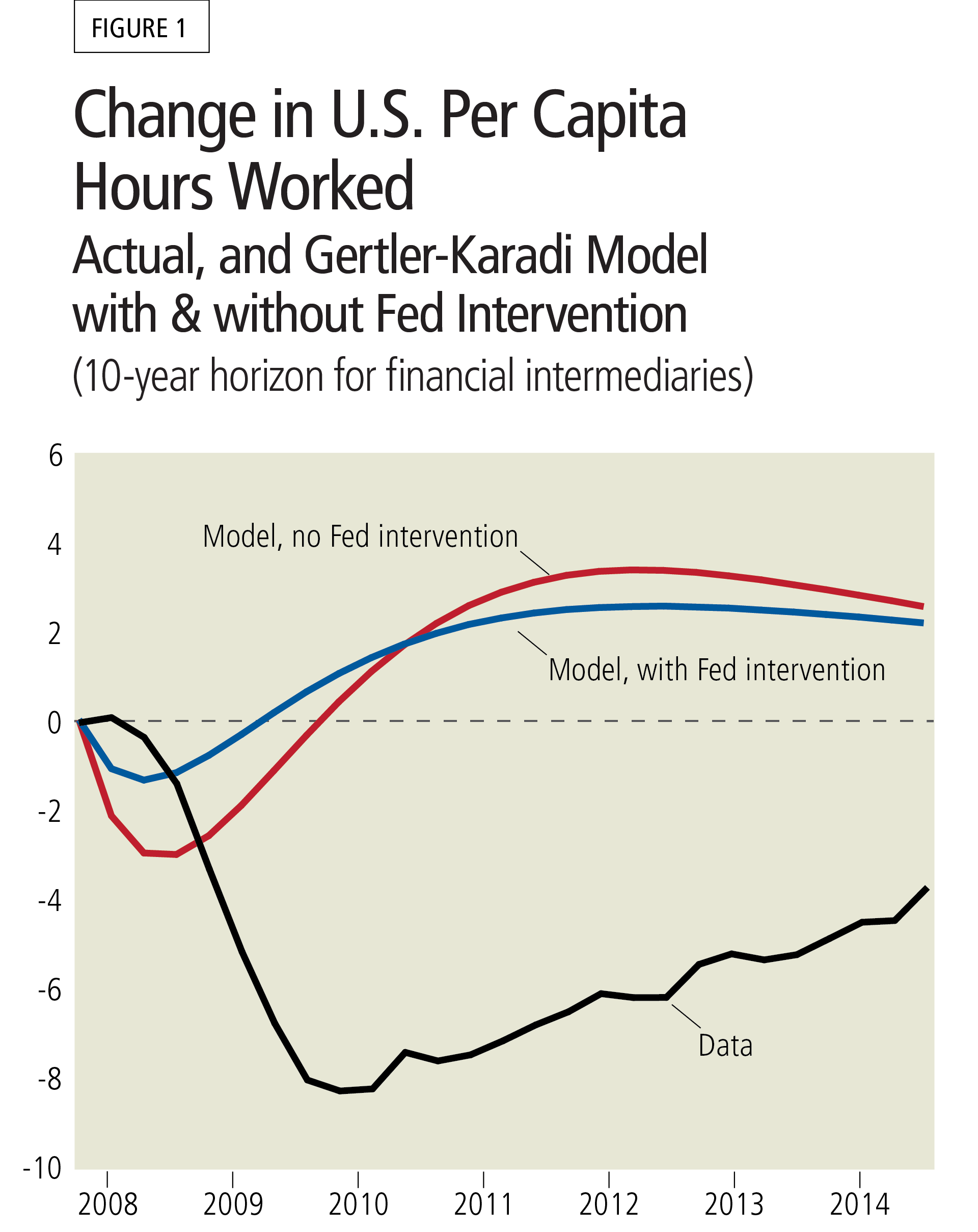

Figure 1 compares U.S. data on per capita hours worked to simulations from the Gertler-Karadi model (2011, fig. 3) with a crisis start of fourth quarter 2007. 4 The three indexes of per capita hours, all set initially at 0, are (1) the model prediction with Fed intervention in credit markets, (2) the model prediction without Fed intervention and (3) actual U.S. per capita hours.

The figure shows (blue line) that per capita hours in the model with Fed intervention falls about 1 percent, recovers and then rises above its initial level. Predicted per capita hours if the Fed does not intervene (red line) shows a fall of close to 3 percent with an even greater subsequent rise. Both model predictions significantly understate the actual decline in per capita hours, seen in the black line. Furthermore, the predicted series recover quickly and rise relative to trend, unlike actual U.S. data.

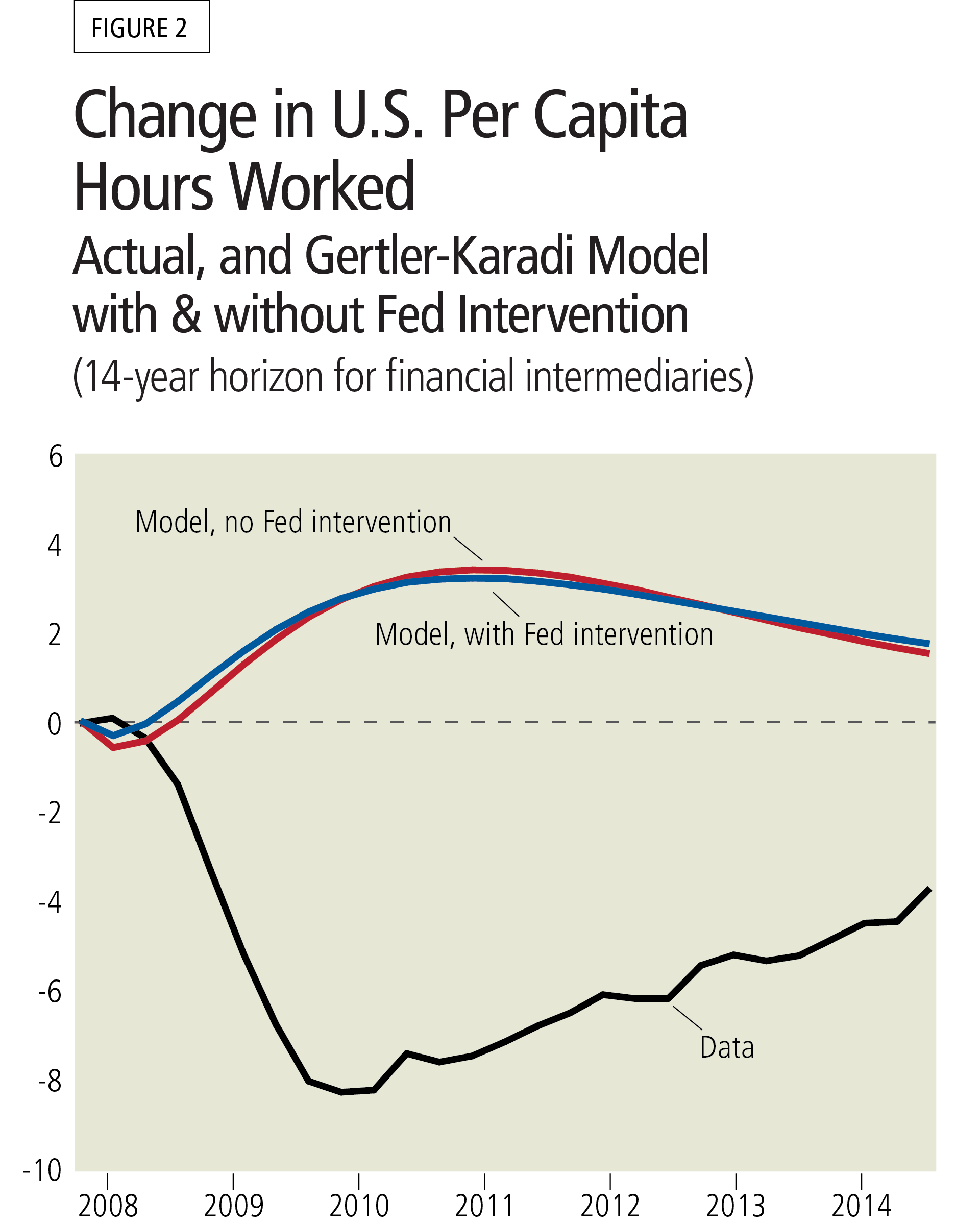

Figure 2 shows the impact of extending the horizon of the financial intermediaries from 10 years to 14 years. With a 14-year horizon, the model predicts a negligible fall in per capita hours at the start of the crisis, followed by a rise relative to trend. Furthermore, with this longer-horizon model, the results with and without Fed intervention are nearly the same, implying that the choice of a banker’s horizon plays a critical role in the analysis. Again, both model predictions significantly understate actual decline in hours. Overall, the predictions of Gertler and Karadi’s model show that Fed policy has little impact on labor inputs, even if we assume that financial intermediaries can divert a large fraction of their assets and are unable to fund much of their investment out of retained earnings.

These negative results from models developed before and after the recent financial downturn lead to the obvious question: If neither conventional nor unconventional monetary policy has significant impact on employment and hours worked, what does? A simple accounting exercise can be used to help find the answer.

Chari, Kehoe and McGrattan (2007) propose an accounting procedure that can be used to develop new theory and determine which factors drive business cycles. My focus here is the downturn of 2008-09.

The procedure has two steps. In the first, Chari, Kehoe and McGrattan (2007) show that the most basic theory can generate the same aggregate time series as those produced by complex theories. This is because we can add “wedges” to the basic theory that look like time-varying taxes and total factor productivity but have no structural interpretation—they simply fill in for whatever factors are actually driving the business cycle. The wedges are chosen to ensure that the time series for the basic model and the more complex models are equivalent.

The point of this first step is to determine which wedges are needed to get equivalence in outcomes between the basic theory and a more complex theory. If those wedges are also needed to account for U.S. time series, then we have found a promising theory.

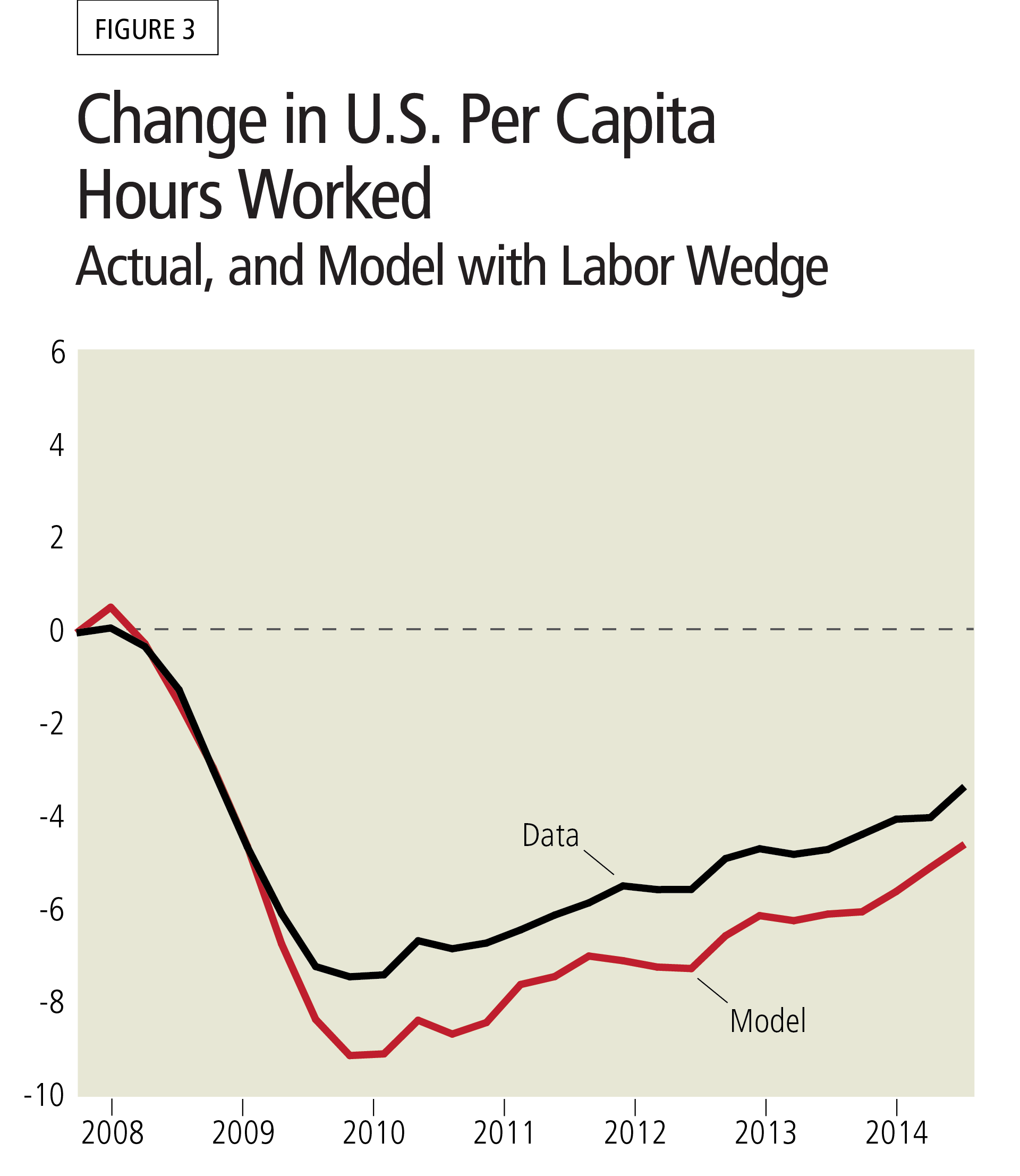

The second step is the accounting that is done using U.S. aggregate data, including data on employment and hours. Specifically, we construct time series for the wedges in the basic theory so that, once they are fed into the model, they generate a match between the model time series and the U.S. time series. Using this procedure with recent U.S. data, we find that one wedge—the “labor” wedge—is all that’s needed to generate a fall in per capita hours that matches actual data. This so-called labor wedge looks like a time-varying tax on labor income. Figure 3 shows U.S. per capita hours of labor—hours per person employed times the number employed—and the predictions of the basic model with a labor wedge added to it. The data (black line) and the model predictions (red line) follow essentially the same path, though the predicted series drops slightly lower than actual data.

Why is this relevant? Because models like those discussed earlier, from Gertler and Karadi (2011) and those surveyed by Gertler and Kiyotaki (2010), focus on factors that disrupt financial markets, such as financial intermediary time horizons, but they do not include factors that distort the labor-leisure decision and thereby generate the labor wedge needed to explain actual fluctuations. 5 Thus, they are not able to account for either the large decline in labor hours and employment during the 2008-09 downturn or the subsequent lack of recovery. Failure to do so indicates that either our new monetary theories do not capture the relevant economic factors driving the data or that monetary actions had little to do with the decline in real activity during this period.

If monetary theories for both conventional and unconventional policies show that Fed interventions have little impact on the labor market, one might ask why the Fed emphasizes employment in its statement of longer-run goals or its regular post-meeting statements. According to Thornton (2011), this emphasis is quite recent. Prior to 2008, Thornton finds that the FOMC “avoided references to full employment or the unemployment rate in stating its policy objectives.” The focus was on price stability and economic growth. Following its meeting on Dec. 15 and 16, 2008, the FOMC’s policy directive mentions the maximum employment objective.

Taylor (2011) uses this fact to argue that the Fed used the full employment mandate to justify discretionary policy rather than rule-based policy advocated by Kydland and Prescott (1977). Focusing only on inflation “wouldn’t stop the Fed from providing liquidity, or serving as lender of last resort, or reducing the interest rate in a financial crisis or recession” (Taylor, 2011). On the other hand, focusing only on inflation would make it more difficult to adopt unconventional policies like credit market intervention. But the results of Gertler-Karadi (2011) suggest that such interventions did little to stimulate real activity.

In this paper, I have reviewed current monetary research, focusing in particular on theoretical predictions for the impact of monetary policy on employment. The main findings suggest that recent accommodative Fed policy had only a small impact on the level of employment relative to the population and there is little the Fed can do to restore the employment-to-population ratio to its pre-2008 level. Proponents of further accommodation are thus faced with the challenge of developing better theories that capture the missing links between monetary policy and employment, evidently factors that drive labor-leisure decisions, rather than links that impact banks and credit markets.

1 Chari, Kehoe and McGrattan (2000) model Fed policy as a monetary growth rule. McGrattan (1999) models Fed policy as an interest rate rule. Both versions deliver the same quantitative results.

2 See Gertler and Kiyotaki (2010) for a nice survey.

3 When computing the impact of Fed policy, Gertler and Karadi (2011) initially assume that bankers have an expected horizon of 10 years and can divert 38 percent of capital. They consider other variations as well. Their model assumes that banks maximize their wealth taking into account that the value of staying in business has to exceed the value of closing the bank and appropriating the existing deposits. This value is affected by shocks to the quality of their assets.

4 Per capita hours worked are calculated as the employment rate times hours worked per employed individual.

5 Technically, Gertler and Karadi’s assumption that there is habit persistence in preferences does generate a wedge, but this factor turns out to be quantitatively insignificant.

Chari, V. V., Patrick J. Kehoe and Ellen R. McGrattan. 2000. “Sticky Price Models of the Business Cycle: Can the Contract Multiplier Solve the Persistence Problem?” Econometrica 68 (5): 1151-79.

Chari, V. V., Patrick J. Kehoe and Ellen R. McGrattan. 2007. “Business Cycle Accounting.” Econometrica 75 (3): 781-836.

Federal Reserve Board of Governors. 2014. “Statement on Longer-Run Goals and Monetary Policy Strategy.”

Gertler, Mark, and Peter Karadi. 2011. “A Model of Unconventional Monetary Policy.” Journal of Monetary Economics 58 (1): 17-34.

Gertler, Mark, and Nobuhiro Kiyotaki. 2010. “Financial Intermediation and Credit Policy in Business Cycle Analysis,” in eds., B. M. Friedman and M. Woodford, Handbook of Monetary Economics, Vol. 3, 547-99.

Kydland, Finn, and Edward C. Prescott. 1977. “Rules Rather Than Discretion: The Inconsistency of Optimal Plans.” Journal of Political Economy 85: 473-90.

Taylor, John B. 2011. “End the Fed’s Dual Mandate and Focus on Prices.” Bloomberg View. September 16.

Thornton, Daniel. 2011. “What Does the Change in the FOMC’s Statement of Objectives Mean?” Economic Synopses. Federal Reserve Bank of St. Louis.